2019 Reflections:

December was a terrific month for our stock holdings, with our typical stock portfolio rising over 12%. The broad stock market produced a solid result too, increasing 2.9%, however, our outperformance is statistically significant.

Our full-year 2019 returns were positive but modest until December as we continued to invest with discipline, committing capital to companies only when the share prices were sharply discounted. Of note was our mid-year investment in Kraft Heinze Company (NASDAQ: KHC). In 2015, Warren Buffett’s Berkshire Hathaway bought 25% of the company for about $52 per share – we established our position in the low $30s range. While KHC closed the year at $32.13 per share, the company pays a dividend of about 5%. We think the shares are substantially undervalued (our appraised value for the company is in the mid-$50 range), and under certain circumstances, we believe Berkshire Hathaway could make an offer to take the company private at a price well above our cost.

We also added several bond positions trading at attractive discounts to par value. While we seem to be finding slightly more attractive investment opportunities in the bond market than in the stock market, we remain alert to compelling investment opportunities in both.

In December, two of the companies we hold saw price increases of over 50% during the month. Another three had returns of between 12% and 20%. Even with that, our overall stock portfolio trades at 53% of our appraised value, implying significant potential for further appreciation. As we have stated, we invest in companies when the last quoted stock price is half of our appraised value. Over time, we expect the gap between the stock price and our appraised value to close. We can’t predict when that will occur, so we continuously monitor and reappraise each company, attempting to identify a triggering event to close the value gap.

Apropos of this, in mid-December, TravelCenters of America (NASDAQ: TA), one of our long-time undervalued holdings, announced a change of its CEO. This catalytic news triggered a share increase of 110% over the course of seven trading days. We believe the stock price is still well below appraised value, even after this large increase.

Our investment discipline requires us to establish a fair or appraised value for each company in which we invest. Our appraisal is determined through rigorous analysis of a company’s financial statements, including its balance sheet, cash-flow statement, and income statement. In addition to reading quarterly and annual SEC filings, company press releases, proxy statements, and industry-related data, we also speak with members of senior management – typically the company’s CFO or CEO (in many cases both). After we calculate an appraised value, we compare it to the stock price. If a large gap exists, that is, the stock trades well below our appraisal, we invest.

At the time we commit capital and make an investment, we have a specific target price in mind – the appraised value. Our goal is to have the gap between the stock price and appraised value close as quickly as possible, producing attractive investment returns. Each day a company operates, it has the potential to increase its value. Over months and quarters of holding a stock, its value can increase or decrease based upon management’s effectiveness in executing its business plan, or for other reasons over which the company may have less control, such as general industry or economic changes. Therefore, our appraised value is subject to modification.

We spend significant time each day reviewing our current holdings. Over time, as we identify companies increasing their value through successful execution of a strategic plan, we observe this is not always immediately reflected in the share price. In fact, our experiences show there is only a casual relationship over the short-term between improving company value and an increasing stock or bond price.

As a company’s value increases, our expected return on investment increases up to the point when the stock price approaches our appraised value and the gap has been closed. For example, if we appraise a company with a value of $50 and invest when the stock trades at $40, we have an expected return of 25%. But if over time our appraisal increases to $60, our expected return increases to 50%.

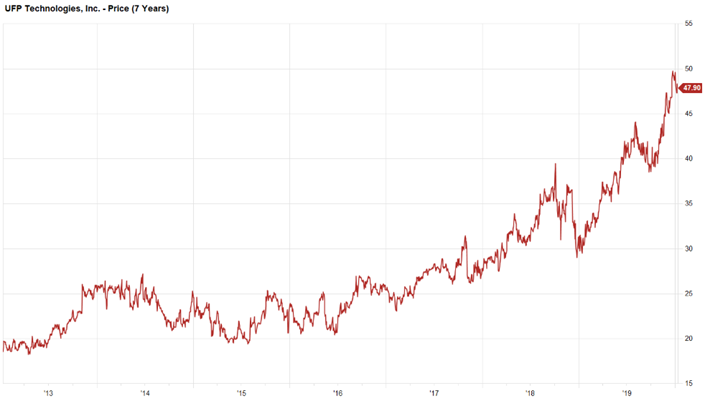

A good example is UFP Technologies, Inc. (NASDAQ: UFPT), a company in which we invested several years ago. UFPT produces specialty packaging for applications ranging from shipping wine bottles to sterile storage of medical instruments. The stock price chart below shows how the price has trended over the past seven years.

When we first purchased the stock, it traded around $16 per share. We appraised the business at that time to be worth roughly $32. Over subsequent periods, as the company matured and management successfully executed its business strategy, including a shrewd acquisition, our appraised value increased. The stock now trades just below $50, and our appraised value has increased to nearly $55 (representing a 244% return on the original purchase price of $16).

A truly successful investment for our firm is one in which the gap between price and value closes over time, but the appraised value continuously increases, allowing for a return on investment of several times our initial investment.

Reflecting back just over a year, you may recall the broad market as measured by the Value Line Stock Index experienced a sharp decline, causing 2018 to end with a thud. Investor sentiment turned negative as a result of threatened trade wars and anticipated interest rate hikes. The fourth quarter of 2018 alone dropped by 19%, including December’s 11% decline. This was a stark reminder that short-term stock prices fluctuate much more than the value of the underlying companies.

The period of investor exuberance that characterized much of 2019 reminds us of the late 1990s, as we were nearing the end of the great tech boom (the dot-com bubble). Investors were capricious, groping for returns. Volatility was high. Company financial results were subordinate to other measures of value, such as the number of daily visitors to a company’s website. IPOs of new companies with zero revenue were common. You may recall names such as eToys.com or Webvan It was during this time Warren Buffett famously stated, “We know what’s going to happen, we just don’t know when.” The following three years were disastrous as the broad equity markets traded down between 50% and 80%, and many unknowing investors suffered significant or permanent loss of capital. Buffet later said, “Risk comes from not knowing what you’re doing,” which was obviously the case for many investors and advisors.

As we look back over the past few years and the way markets have traded along with central bank policies and global economic trends, we are reminded of another of Buffett’s comments, “Do not take yearly results too seriously. Instead, focus on four or five-year averages.” We remain disciplined in our investment approach, knowing over time stock prices tend to reflect underlying company value. We hold a concentrated selection of stocks and bonds, that, taken as a group, trade for just over 50% of our appraised value. We are emerging from a lackluster period and believe the best times for us and our clients are ahead. If December is any guide, the future looks very promising and we expect to see the gap between price and company value close. Recall that price is what you pay, and value is what you get; the risk in investing is the risk of paying too much. We remain committed to investing only when prospective investment meets our strict valuation criteria.

Portfolio:

The accelerated level of economic and political uncertainty has created a more attractive investment environment. Over the past few weeks the Dow Jones Industrial Index has had numerous days in which it swung from negative to positive and back again, moving several hundred points or more. We appreciate price variability and the irrational behavior it begets as this leads to the short-term mispricing of stocks and bonds. We remain confident in the securities we hold, our investment strategy, and our rigorous analytical process. Although the prices of many of the companies we hold remain depressed, we see through the short-term price volatility to discern the long-term value of the underlying businesses. This is where our analytical process focus is – not the last quoted stock price.

Equity:

AutoWeb, Inc. (AUTO)

A US-based automotive marketing services company providing high-quality consumer leads, internet advertising, and associated marketing services to automotive dealers and manufacturers throughout the United States. The company’s products include new and used vehicle lead generation programs, which allow consumers to submit requests for pricing and availability of specific vehicle makes and models within a geographic area, and online advertising programs including impression-based and click-through ads. Management has developed and is executing a strategic plan that we expect will lead to meaningful value creation. A normalization of revenues and margins should cause AUTO to trade in line with historic multiples. The share price remains well below our appraised value.

Core Molding Technologies, Inc. (CMT)

A US-based manufacturer of sheet molding compound and various fiberglass- and plastic-based heat-molded products. The company’s customers include manufacturers of heavy-duty trucks, automobiles, personal recreational vehicles, and a variety of consumer and industrial goods that incorporate high-strength molded components. CMT recent acquired Horizon Plastics, a Canadian manufacturer of high-strength structural plastic components; the combined company presents attractive synergistic opportunities. CEO David Duvall is leading an operational turnaround that focuses heavily on manufacturing efficiencies; early results are evident. The company has operations throughout North America. The share price remains well below our appraised value.

Corning Incorporated (GLW)

A US-based global manufacturing business that produces display glass, fiber optic cables, emission control products, medical and pharmaceutical equipment, and specialty glass. Widely known products include Gorilla Glass, a durable display glass used in mobile electronic devices, and Valor Glass pharmaceutical vials, in which the company is investing heavily. GLW is among the foremost providers of fiber optic cables, which will play an increasingly important role in continuing development of global telecommunication infrastructure. GLW’s business has improved over the past few years, narrowing its market value compared to our appraised value, but growth opportunities remain.

Flexsteel Industries, Inc. (FLXS)

A US-based manufacturer of wooden, metal, and upholstered furniture. Short-term trade concerns and disruptions stemming from the partial implementation of a new business information system have caused consternation among market participants. The company has implemented and is executing a comprehensive turnaround plan. We expect FLXS to recover lost revenue, implement control costs, rationalize its operating footprint, and return to its previous margin profile. The company has a strong cash position and no debt. New CEO Jerry Dittmer brings significant industry experience and managerial knowledge. FLXS will continue to play a role in fulfilling the need for furniture across a range of price points while adapting to changing customer preferences. The share price remains well below our appraised value.

Update: We attended the annual meeting of shareholders in Minneapolis in early December, expressing our views related to strategy and execution to the entire board of directors. We also enjoyed a one-on-one meeting with the CEO and Board Chairman in advance of the meeting which was constructive and allowed us to share specific thoughts on how to increase shareholder value.

Fluent, Inc. (FLNT)

A US-based digital marketing business offering performance-based marketing solutions through targeted digital interactions. FLNT is growing rapidly, and we anticipate that investors will soon appreciate the business’s healthy margins and cash generation potential, resulting in significant price appreciation. Excesses cash from operations may be used to prepay debt or for accretive acquisitions. The company possesses a desirable competitive position, unique products, and a young and innovative workforce. We maintain a high degree of confidence in Fluent’s management team. The share price remains well below our appraised value.

Update: The company presented to investors at the Needham Research conference and provided updates to its previous revenue and margin guidance. The update was favorably received and prompted a sharp increase is share price.

Gulf Island Fabrication, Inc. (GIFI)

A US-based fabricator of complex steel structures for customers in the oil and gas industry. GIFI also fabricates marine vessels, including tugboats, offshore supply vessels, civilian transportation vessels, and government vessels. The company is well-positioned to participate in a developing US offshore wind energy market and the ongoing development of petrochemical processing capacity on the US Gulf Coast. GIFI has a strong liquidity position after rightsizing its physical footprint, and trades at only a slight premium to net cash per share. Recent changes to the board of directors and executive management will provide fresh perspectives on capital allocation commensurate with GIFI’s fluid end markets. We expect continued growth in backlog and improved execution will result in meaningful price appreciation. The share price remains well below our appraised value.

Update: The company appointed a new CEO, Richard Heo, who brings significant industry and operational experience to the company. We remain actively engaged with management and the board who have been receptive to shareholder input and strategies to drive the stock price higher.

Kraft Heinz Company (KHC)

A US-based diversified manufacturer and marketer of food and beverages products. In 2015, Warren Buffett’s Berkshire Hathaway and investment firm 3G Capital orchestrated the merger of Kraft Foods and H.J. Heinz; the two investment firms hold a combined equity position in KHC of nearly 50%. Aggressive cost cutting after the merger led to an underinvestment in legacy brands, resulting in an impairment of goodwill in early 2019. Market sentiment is decidedly negative, but we believe KHC’s business is fundamentally sound. Recently appointed CEO Miguel Patricio has taken a measured approach to brand development and rationalizing KHC’s product portfolio, which we expect to be a catalyst to value creation. The share price remains well below our appraised value.

Update: Patricio provided a glimpse of the soon to be announce strategic plan for the company during an interview with the Wall Street Journal. KHC will focus on fewer, bigger opportunities. Operational details will be released during Q1.

LSB Industries, Inc. (LXU)

A US-based producer of nitrogen-based agriculture and industrial products at three owned facilities and one non-owned staffed plant. Ongoing changes to operational and maintenance procedures have meaningfully improved onstream rates. Growth opportunities exist in both the cyclical agricultural fertilizer segment and the high-margin industrial and mining segment. Historical executional issues are fading from the market’s memory, although the company’s capital structure is heavily weighted towards debt. We expect further balance sheet strengthening as cash flow improves. Coupled with continued operational reliability, this should lead to significant stock price appreciation. The share price remains well below our appraised value.

New York Community Bank, Inc. (NYCB)

A US-based mid-tier consumer and commercial bank offering deposit and loan products and services. NYCB has established a niche lending position in the rent-controlled multi-family housing market in New York City and has recently shown growth in its specialty commercial financing business. Loan loss provisions and actual write-offs are substantially and consistently among the lowest in its peer group. Recently legislation raised the threshold that defines a Systematically Important Financial Institution (SIFI) from $50 billion to $250 billion. NYCB has resumed growth after several stagnant years and we remain optimistic about the potential for it to acquire another bank or be acquired. The share price remains below our appraised value.

Seaspan Corporation (SSW)

A Hong Kong-based, globally operated independent owner and manager of oceangoing container ships which are chartered on long-term, fixed-rate time charters to various established container liner companies. Market recovery from a period of depressed charter rates due to an oversupply of vessels is underway. We believe industry and economic conditions remain favorable in the medium- to long-term. SSW recently announced the acquisition of APR Energy, a global leader in specialized power solutions; we believe the combination is sensible and will be accretive to shareholders. SSW is planning to convert to a holding company structure and adopt the corporate name “Atlas Corp.” to reflect its newly diversified business structure. The share price remains below our appraised value.

Update: Announced the acquisition of a mobile energy business that adds a new and differentiated operational division to the company which will reorganize into shipping and energy units. The company will rename itself Atlas Corp.

StealthGas Inc. (GASS)

An Athens, Greece-based, globally operated shipping company that provides seaborne transportation of liquified petroleum gas (LPG). GASS is dominant in the small-sized pressurized LPG shipping market, which continues to improve with accelerating demand for product transportation and a favorable outlook for global fleet growth in the segment. We believe GASS is trading at an attractive discount to net asset value and has significant appreciation potential. The share price remains well below our appraised value.

Update: Announced the acquisition of four medium size LPG tankers from a privately held German company, adding to its expanding fleet in the mid-sized shipping class.

Subsea 7 S.A. (SUBCY)

A London, England-based, globally operated company providing seabed-to-surface engineering, construction, and services to the offshore energy industry. SUBCY’s stock was disproportionately discounted during a period of reduced offshore oil and gas exploration and production activity but has benefitted from improving markets and normalizing capital expenditures by its customers. The acquisitions of Seaway Heavy Lifting and Siem Offshore Contractors have provided exposure to the growing offshore renewable energy market. SUBCY’s technology portfolio is among the best in its industry, and its balance sheet is nearly debt-free. The share price remains below our appraised value.

Update: Long-standing CEO Jean NAME announced an expected resignation effective December 31st, passing the baton to NAME to lead the business into the next decade.

TravelCenters of America Inc. (TA)

A US-based business that owns, operates, and franchises travel centers offering refueling, dining, and ancillary travel services to truckers and motorists. Properties are concentrated along the US interstate highway system and larger state highways. A renewed focus on expansion through franchising coupled with improvements in servicing capabilities position the company for revenue growth and margin improvement. The company’s portfolio of unique assets has substantial intrinsic value. A recent management change was received enthusiastically by shareholders. The share price remains below our appraised value.

Update: Announced CEO change that brings Jonathan Pertchik to the helm to continue building the business as it executes it TA-Express business expansion. Pertchik is an experienced executive who has led multiple businesses in different industries through various stages of transformation over the past 20 years. We remain actively engaged with the company sharing our views on value creation.

UFP Technologies, Inc. (UFPT)

A US-based designer, engineer, and producer of high-grade foam and molded fiber solutions for electronic, medical, and specialty packaged products. A disciplined management team has consistently executed on growth and efficiency initiatives, driving long-term shareholder value. The recent acquisition of Dielectrics increases exposure to fast-growing medical markets, and we anticipate similar accretive transactions in the future. We believe there is additional share price appreciation potential.

Wayside Technology Group, Inc. (WSTG)

A US-based, globally operated technology wholesale company that distributes computer software and hardware developed by others, as well as provides technical and related customer services. Top-line growth has been consistent but net margins have been compressed. Changes implemented by management hired within the past two years are beginning to bear fruit, and we expect bottom-line growth continue and accelerate. The share price remains below our appraised value.

Update: Promoted Dale Foster to CEO and Board member from his prior role of divisional President. Foster will continue building on recent strong revenue and earnings growth as the company executes its strategic growth plan.

Debt:

CoreCivic, Inc. 4.75% due 10/15/2027 (21871NAA9)

Operates as a solutions provider to state and federal governments primarily to ease the burden of overcapacity of existing corrections facilities, detention centers and state and federal prisons. CXW also builds and operates office buildings for various government agencies. The company recently announced additional investment in real estate operating assets as well as two new service contracts, all expected to improve operating cash-flow.

This bond was added during the fourth quarter while trading in the $85 price range, providing an attractive total return over its remaining eight-year life. The current yield at cost is over 5.50%. We view this as an underappreciated company with attractive economic characteristics that provides consistent cash-flows to service its debt.

GE Capital Corporation VRN due 3/15/2023 (36966THT2)

A global technology and financial services company that develops and manufactures products for the generation, transmission, distribution, control and utilization of electricity. Its products and services include aircraft engines, power generation, water processing, security technology, medical imaging, business and consumer financing, media content and industrial products.

The variable rate provides a hedge against rising interest rates while maintaining a short duration.

We expect GE to focus on deleveraging its balance sheet though asset sales and restructuring.

Kraft Heinz Food3.00% due 6/1/2026 (50077LAD8)

A US-based, globally diversified manufacturer and marketer of food and beverages products. In 2015 Berkshire Hathaway and investment firm 3G Capital orchestrated the merger of Kraft Foods and H.J. Heinz; the two firms hold a combined equity position in KHC of nearly 50%. Aggressive cost cutting after the merger led to an underinvestment in legacy brands, resulting in an impairment of goodwill in early 2019. Market sentiment has improved under the leadership of recently appointed CEO Miguel Particio. We believe KHC’s business is fundamentally sound. We anticipate improved cash generation will allow KHC to refinance its debt while continuing to deleverage its balance sheet.

Owens & Minor, Inc. 4.375% due 12/15/2024 (690732AE2)

A US-based company that engages in provision of services to the manufacturers of healthcare products, supplies, and devices. It operates through the Global Solutions and Global Products segments. The Global Solutions segment includes United States and European distribution, logistics and value-added services business. The Global Products segment manufactures and sources medical surgical products through production and kitting operations. A 2019 mid-year change in executive management has resulted in improved financial performance and greater profitability and cash-flow. A recent sale of non-core European assets will allow for balance sheet improvement and greater focus on its core US business. We anticipate the company will restructure its balance sheet and participate in ongoing industry consolidation.

Pitney Bowes Inc. 4.95% due 4/1/2023 (724479AN0)

A US-based, globally focused technology company which engages in the provision of products and solutions in the commerce industry. It offers information management, location intelligence, and customer engagement products and solutions and also provides shipping, mailing, fulfillment, returns and cross-border ecommerce products and solutions that enable the sending of parcels and packages across the globe. We believe the company will be acquired in a private equity transaction that will privatize the business. The company continues to shed non-core business and use the proceeds to strengthen its balance sheet.

Trinity Industries, Inc. 4.55% due 10/1/2024 (896522AH2)

A US-based company that engages in the provision of rail transportation products and services in North America. It operates through the following segments: Railcar Leasing and Management Services Group, Rail Products Group and All Other. The company recently split into two businesses as part of its long-term restructuring plan which improved its balance sheet and operations. We expect the price of this bond to improve as the underlying business strengthens. Value Act Capital recently increased its equity ownership to 20.9%, foreshadowing a go private transaction.

United States TIPS 0.375% due 1/15/2027 (912828V49)

A direct obligation of the government of the United States of America, with the largest economy in the world having annual economic production in excess of $20 trillion. Returns on TIPS are bifurcated into semi- annual interest payments and an appreciation in the corpus that reflects the sum of headline inflation, as measure by the US Consumer Price Index (CPI), over the life of the bond. We anticipate future accelerated inflation and use TIPS as a hedge.

United States TIPS 1.75% due 1/15/2028 (912810PV4)

A direct obligation of the government of the United States of America, with the largest economy in the world having annual economic production in excess of $20 trillion. Returns on TIPS are bifurcated into semi- annual interest payments and an appreciation in the corpus that reflects the sum of headline inflation, as measure by the US Consumer Price Index (CPI), over the life of the bond. We anticipate future accelerated inflation and use TIPS as a hedge.

Cash Equivalents:

We continue to hold above average amount of cash reserves in portfolios. We have done so for the past few years as we’ve patiently waited for better valuations.

To improve returns on cash holdings, we’ve been investing in 90-day Treasury Bills. Every 30 days we roll over a new T-Bill so that over a three-month period we end up holding a 30, 60 and 90-day T-Bill, creating a ladder of liquidity.

T-Bills are direct obligations of the US Government and arguably the safest, most liquid asset in the world. We invest in T-Bills due to their safety and return characteristics – our last three T-Bill investments are returning 1.55% annualized, down slightly from recent yields. This compares to an average annualized yield of 0.09% and 0.15% on FDIC-insured savings account and interest-bearing checking account, and 0.15% on the average national money market fund. We continue to earn a premium return on cash.

From Our Library:

Our research team has been reading Accounting For Value by Stephen Penman. This is a technical book covering financial statement analysis and contemporary finance teachings. Penman offers insightful perspective on ambiguities inherent in GAAP accounting rules and how some companies exploit those, offering advice to better appraise a company’s real intrinsic value:

Active fundamental investing rests on the notion that prices can deviate from fundamentals but ultimately return to fundamental value. The idea is that fundamental value will ultimately be revealed and become obvious to the market through credible information arriving at the market. If the [company’s] accounting is non-speculative, as the fundamentalist desires, the correcting information comes through the firm’s financial statements. Earnings drive stock prices, so the fundamentalist focuses on “long-run earnings power” with the recognition that prices will adjust to earnings information as it arrives.

… fundamental investors know this well. They could see that the expectations implicit in the prices of dot.com firms was unreasonable, but their sell positions in 1997 seemed increasingly foolish as the momentum continued. Patience was ultimately rewarded, however, as the sales and earnings anticipated by market prices failed to materialize in financial reports.

For the long-term trader, patience is required, for prices that deviate from fundamentals can deviate even more before they gravitate. As in life, patience is always tested.

Firm Update:

We completed our move from Mequon, WI to our new Milwaukee downtown location. Please feel free to drop by if you’re in the area.

We have a new associate joining our Indian subsidiary office, Naveen Kumar. His first day will be February 3rd. He joins us from FactSet, a leading financial industry data and information gathering company, and will work with our fundamental research team in Hyderabad, India. We are excited for him to join us and share his industry experience.

Concluding Thoughts:

As we continue to navigate through this period of uncertain geopolitics and unprecedented central bank monetary policy, we assure you our investment discipline and commitment to those principals remains intact. It is through the certainty and consistency of our investment process that we are confident in future results and our expectation of superior investment returns.

We are grateful to clients for the trust and confidence placed in us to act as stewards of their investment capital.

Your Investment Research and Advisory Team

Global Value Investment Corp.