Market Update & Economic Summary:

The year began with significant price volatility. This came as no surprise given the continuing uncertain global economic environment. Consider this, the Central Bank of Japan elected to set interest rates at negative levels in mid-January; in March the European Central Bank further reduced rates into negative territory, a strategy employed since June of 2014; and recently US Fed Chairwoman Yellen indicated any near-term rate increase was likely off the table, telegraphing signs of a weaker US economy despite eight years of accommodative policy and almost four trillion dollars of Fed balance sheet expansion.

A few issues confounding market pundits are the strength of the US dollar, which has negatively impacted US competitiveness around the world, as well as the persistent low levels of inflation which central bankers have been furiously attempting to reverse. The US rate of inflation has consistently been between 1 and 2 percent. The Fed would like this to be above 2% to insure consistent modestly rising prices.

US GDP grew at 1.4% in the fourth quarter of 2015. Relative to the past few years this is a solid number. Relative to the post WWII period average of 3.25% it’s still too low. Some would argue as the economy approaches $18 trillion it is harder to grow at that historic rate, but a mere 2-3 years ago the economy had a series of quarters of 4% growth. In other words, to assume the economy can grow at 3% plus, or double its current rate, is realistic.

One of the biggest recent factors driving market share price volatility has been energy. Oil prices have behaved predictably over the past 18 months, as global supply exceeded demand, price declined. Oil traded as high as $110/barrel in mid-2014 then declined to a recent low price of $26.05/barrel. In a market based economy price equilibrium is reached when supply = demand. At the moment supply exceeds demand thus price has declined. Economic theory states prices will move to a level where either demand increases or supply decreases. The US has experienced a production contraction as witnessed by the sizeable number of newly unemployed energy industry workers. Domestic production is currently 9 million barrels per day, down from 9.7 million in April of 2015. In the long run the path to higher price is not through supply cuts, but rather through increased demand which we believe will occur as the global economic rate of growth returns to historic levels. In the absence of increasing demand, we suspect oil prices will remain in its recent range of $25-$40/barrel.

The US unemployment rate ticked up to 5.0% from 4.9% when reported on April 1st. Of greater importance is the labor force participation rate which edged up to 63%. Although the US employment picture is improving, average hourly pay remains muted. With recent legislatively induced minimum wage increases in California and New York, we would expect to see improving wages and potentially renewed wage inflation.

During the 1st quarter stock market benchmarks were mixed as the DOW 30 rose +2.1%, the S&P 500 gained +1.4% and the Value Line Even Weight index was up +1.8%. Foreign markets didn’t fare as well as the Stoxx Europe 600 declined -7.7%, and the MSCI EAFE International index fell -3.7%.

US markets experienced extreme volatility between Jan 1st and Feb 11th trading down nearly 14% before staging a strong comeback through March 31st.

Our firm has been cautiously optimistic over the past few years. Recent volatility was welcomed and allowed us to invest in several companies at very attractive prices.

Many stock market participants have taken a notably more negative view over the past few months. This has resulted in more companies having sharply undervalued share prices.

Investment Strategy:

In our year-end 2015 letter we made the following statement:

Our firm concentrates on investing in shares of companies when we can buy a dollar of business for 50 cents. The value of a company’s stock fluctuates far more than the value of the company itself.

We offered several retrospective illustrations in which shares prices of companies had declined sharply and then increased dramatically creating wonderful results.

We went on to say the following:

We believe outsized return-on-investment can be achieved as a consequence of inherent inefficiencies in the public marketplace. The biggest unknown in our strategy is the timing of the realization of our return. We do know from experience that share prices tend to move dramatically over short periods so the ultimate recognition of return may occur very rapidly.

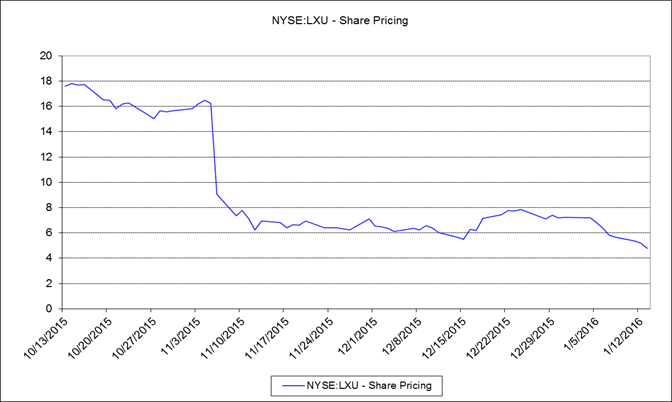

We then offered a contemporary example of a company whose share price had fallen to levels that seemed irrational. This is the graph we provided:

At the time of our letter, LXU’s share price was $5.18. As we anticipated, LXU affected its reorganization, senior management executed its strategy, and the company communicated clearly with market participants demonstrating through their actions how they were creating value for shareholders.

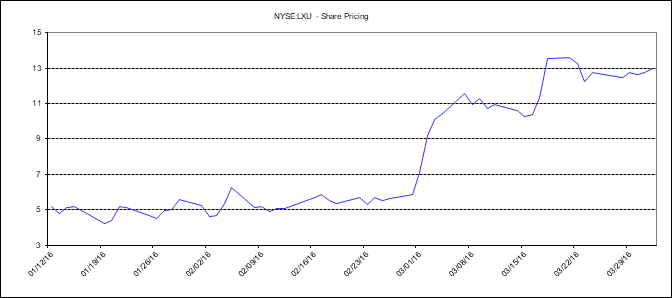

Below is a chart showing how the share price changed since January 12th, closing April 1st at $12.96.

This is another example of how shares of a publicly traded company were available for purchase at a discount and shortly thereafter trading significantly higher. Patient investors can earn attractive return-on-invested capital over time if they are able to identify when shares are trading at undervalued levels as pointed out with this timely example.

Our firm’s research associates spend the majority of their working day analyzing the value of companies. As previously discussed, we study company financial statements and are able to base our appraised value on empirical data. We have found share prices often move without any reason connected to the actual business and are often driven by the emotional disposition of the most reactive investor.

Our goal is to invest when we believe shares are trading at a 50% discount. We measure investment outcomes over years not days. We believe any shorter perspective encourages speculative trading behavior.

We thoroughly research, analyze and establish realistic price targets for each company in which we commit capital. Our research teams regularly communicate with senior management and review financial releases. We update our analysis as additional information becomes available. This process has been developed over many years and is the cornerstone of our investment strategy.

We recognize there is not a good comparative benchmark against which to measure ourselves because we manage money for clients the same way we mange for ourselves, being fundamentally averse to permanent loss of capital and only willing to commit capital when we find suitable investments. We are indifferent to the size of a company, its economic sector, its geographic locations, and other fashionable metrics. We simply concentrate on the current gap between our appraised value and the last quoted share price, and are willing to hold cash while we wait for bargains to appear.

During any given period, whether a calendar quarter or a year, we rarely produce results matching a market benchmark. We accept when we choose to manage money differently, we will predictably achieve different results. Over time we expect to achieve significantly different and superior results.

Firm Update:

We have a few updates to report. The firm was renamed and reorganized in mid-2015 to more accurately reflect the scope of our work and the increasingly global nature of our research and advisory. We created a holding company structure in which Global Value Investment Corp. acts as the parent to its operating divisions Milwaukee Private Wealth Management, Milwaukee Institutional Asset Management, and Global Value Research Company. This structure allows for employee stock ownership in the firm, creating an opportunity for all associates to participate in our success.

Milwaukee Institutional Asset Management was established to work with other investment professionals. We’ve had success in developing professional relationships with other firms which we believe reflects their desire for our unique and disciplined investment strategy.

You can now see our investment profile and results by searching on Morningstar. We began reporting publically last year. Morningstar is an independent analytics firm providing opinions on thousands of mutual funds and investment companies like ours. We are tracked under the Global Value Investment Corp. Total Return Value Strategy. Our website continues with timely updates at www.gvi-corp.com.

Annually we mail clients our Privacy Policy which is included. Let us know if you have questions.

Finally, we want to recognize the excellent analytical work being performed by our three man team in India. Sunil Keshetti, Anand Bandi and Prakash Goath have become an important part of the GVIC team, communicating daily with us through video conference calls. They begin their work day as we are turning off the office lights, allowing us to share unique global perspectives and experiences as well as assimilating news and information flow on a near 24 hour basis.

Concluding Thoughts:

Over time our firm has become more and more adept at exploiting inefficiencies in market pricing. We continue to participate in the capital markets as ongoing uncertainties inevitably creates investment opportunity. Each day we seek to identify situations in which we can invest our capital and the capital entrusted to us by clients. For this we are thankful and continue working with great enthusiasm.

Very best wishes,

Your Investment Research and Advisory Team

Global Value Investment Corp.